How to Get a Mortgage - Home Loans, Land Loans, and Refinancing

Buying a house or land is often a challenging task. Before signing a sales contract, you often need to make careful calculations, thorough research, and a lot of paperwork. Whether you are going to buy a lot or a house, everything usually starts with getting a mortgage or initiating a deed of trust, though the latter is becoming less common these days.

Different Types of Mortgages in the USA

The answer to the question “How to get a mortgage?” often depends on the type of loan you prefer. Mortgage loans can usually be divided into several categories according to their rate type:

-

Fixed-Rate Mortgages. The interest rate for this loan remains the same for the entire loan period. It is predictable but usually starts with higher interest rates than other types of mortgages;

-

Adjustable Rate Mortgages (ARM). This type of loan normally starts with a fixed interest rate, then the rate applied on the balance is adjusted throughout the life of the loan, usually every year, but sometimes monthly.

-

Balloon Mortgages. Your monthly payments are lower but at the end of the loan, you need to pay a large balloon payment. This type of loan requires developing an amortization schedule.

When going through your options, consider choosing between a conventional and a government-insured loan. The main difference between these two types is that the first one is not guaranteed by the federal government. Government-insured loans include:

- Federal Housing Administration mortgage insurance program, also known as FHA insured loans;

- Department of Veterans Affairs loan program that offers the VA loans to military members and their families;

- United States Department of Agriculture (USDA) loan program managed by the Rural Housing Service (RHS). They offer USDA/RHS loans for country borrowers who meet specific income requirements.

Another distinction is based on the amount you want to borrow. Choose between:

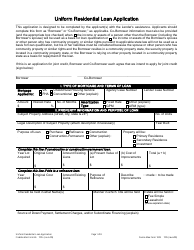

- A conforming loan - the loan that falls within limits set by two government-controlled corporations, Freddie Mac and Fannie Mae. Freddie Mac Form 65/Fannie Mae Form 1003 is normally used to apply for this loan;

- A jumbo loan is a loan with non-conforming loan limits. It is common in high-cost areas and you must have excellent credit to apply for this mortgage.

What Are the Pros and Cons of a Mortgage?

Most people are nervous when it comes to submitting their application. Consider all of the pros and cons of a mortgage before continuing with the paperwork:

Pro: Loans help make home ownership affordable. Instead of paying rent or buying a tiny house (which is a rather complicated task considering United States laws), you can pay for your own full-fledged house on a monthly basis. What’s more, it is a good investment;

Pro: Mortgage interest rates are usually lower than most of the other forms of borrowing;

Con: There is are risks of a potential foreclosure. If you run into any unexpected financial troubles, you may risk losing your property. To prevent it, you can use a mortgage relief program that offers you several ways to help you mitigate your mortgage debt, like refinancing or break in payments;

Con: Monthly payments may change if you have chosen an ARM.

How to Get a Loan for a House?

Buying a house is best done through a pre-approval for a mortgage. Pre-approval will help you to figure an amount you can depend on when looking for a house. Make thorough calculations while choosing a home mortgage to avoid potential foreclosure. Besides, you may want to choose how you will own your property beforehand. If you are married, you may want to arrange joint ownership. Creating a deed that includes your spouse and children can be an effective option.

After the financial institution has decided that you qualify for a mortgage, you will need to have your new home appraised. The next step will be ordering a home inspection. If the inspection finds serious damages, you can ask for a repair or for lowering the house price. While buying a house, you will have to deal with a lot of documents, like warranty deed, by which the seller will guarantee the house is free of encumbrances, or a flood certification that will state the flood zone status of your property. Hire a specialist that will help you to handle the process to avoid any misunderstandings.

How to Get a Mortgage for Land?

If you have decided to buy land and build a house, you will notice that the general process of getting a mortgage for land purchase is very similar to that of a home mortgage. You have to prove your excellent credit, consistent income and have an acceptable debt-to-income ratio. However, you can face some unexpected difficulties. First of all, the land loan is considered a riskier business for the lender. That results in higher land mortgage rates and down payments compared to home mortgage rates.

The process of getting a land mortgage may depend on the location and your plans for the land. If you have a solid plan that states you buy land for commercial use or for building a home, it may highly increase your chances to get a loan. In addition to the above-mentioned categories, the land loans can be divided into:

- Raw Land Loan. You buy land that has no improvements, like electricity or roads;

- Lot-Land Loan. The land you buy already has some basic infrastructure;

- Construction Loans. It allows you to cover the expenses for land purchase and construction with one loan.

The best way to get a land loan and not pay too high-interest rates is to consider one of the USDA/RHS loans.