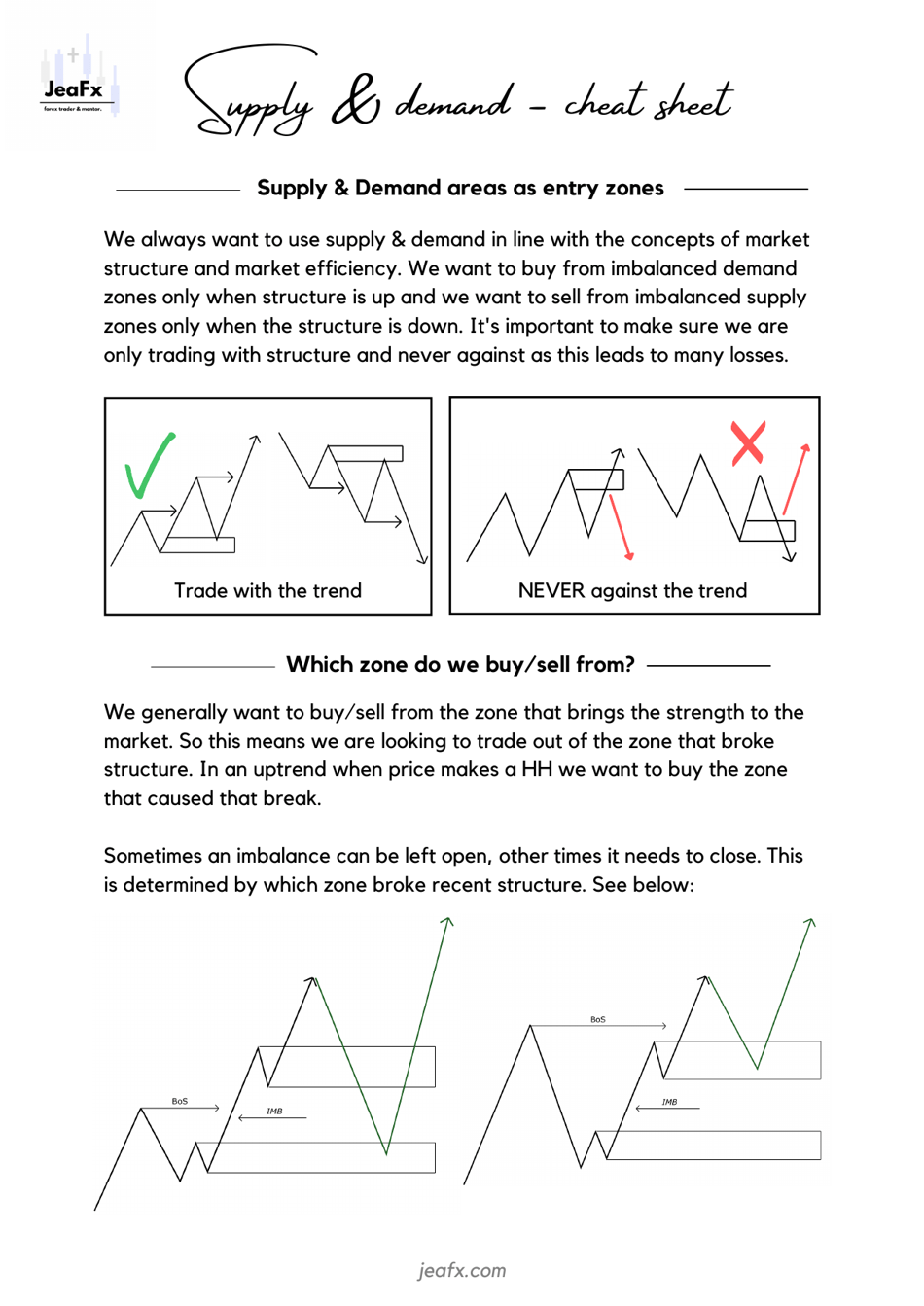

Supply & Demand Cheat Sheet

The Supply & Demand Cheat Sheet is a quick reference guide that explains the basic concepts of supply and demand in economics. It helps individuals understand how the availability of a good or service (supply) and the desire or need for that good or service (demand) interact to determine the price and quantity in a market.

FAQ

Q: What is supply?

A: Supply refers to the quantity of a product or service that producers are willing and able to provide.

Q: What is demand?

A: Demand refers to the quantity of a product or service that consumers are willing and able to purchase.

Q: How do supply and demand interact?

A: Supply and demand interact to determine the equilibrium price and quantity of a product or service in a market.

Q: What is the law of supply?

A: The law of supply states that as the price of a product or service increases, the quantity supplied by producers also increases.

Q: What is the law of demand?

A: The law of demand states that as the price of a product or service decreases, the quantity demanded by consumers increases.

Q: What is equilibrium price?

A: Equilibrium price is the price at which the quantity demanded and the quantity supplied are equal.

Q: What happens when there is a surplus?

A: A surplus occurs when the quantity supplied exceeds the quantity demanded, leading to downward pressure on the price.

Q: What happens when there is a shortage?

A: A shortage occurs when the quantity demanded exceeds the quantity supplied, leading to upward pressure on the price.

Q: What factors can affect supply?

A: Factors that can affect supply include the cost of production, technology, government regulations, and the number of producers in the market.

Q: What factors can affect demand?

A: Factors that can affect demand include consumer preferences, income levels, population size, and the price of related goods or services.

Download Supply & Demand Cheat Sheet

1

2