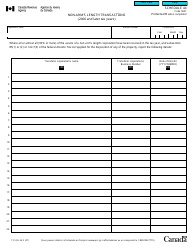

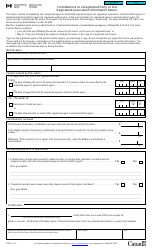

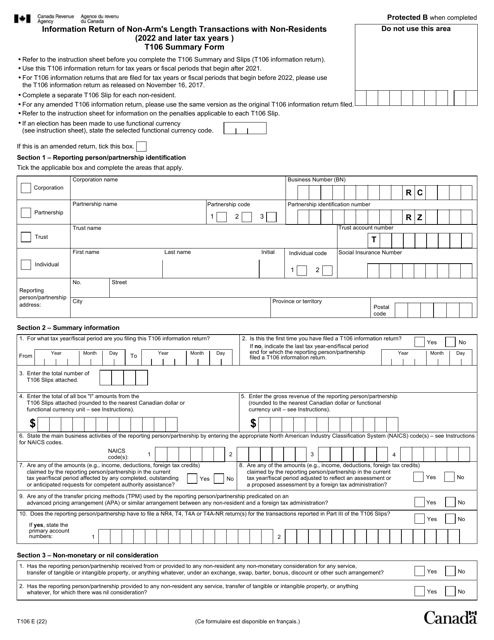

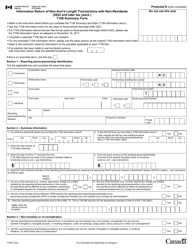

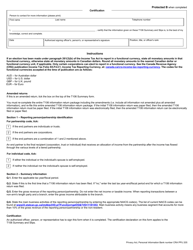

Form T106 Information Return of Non-arm's Length Transactions With Non-residents (2022 and Later Tax Years) - Canada

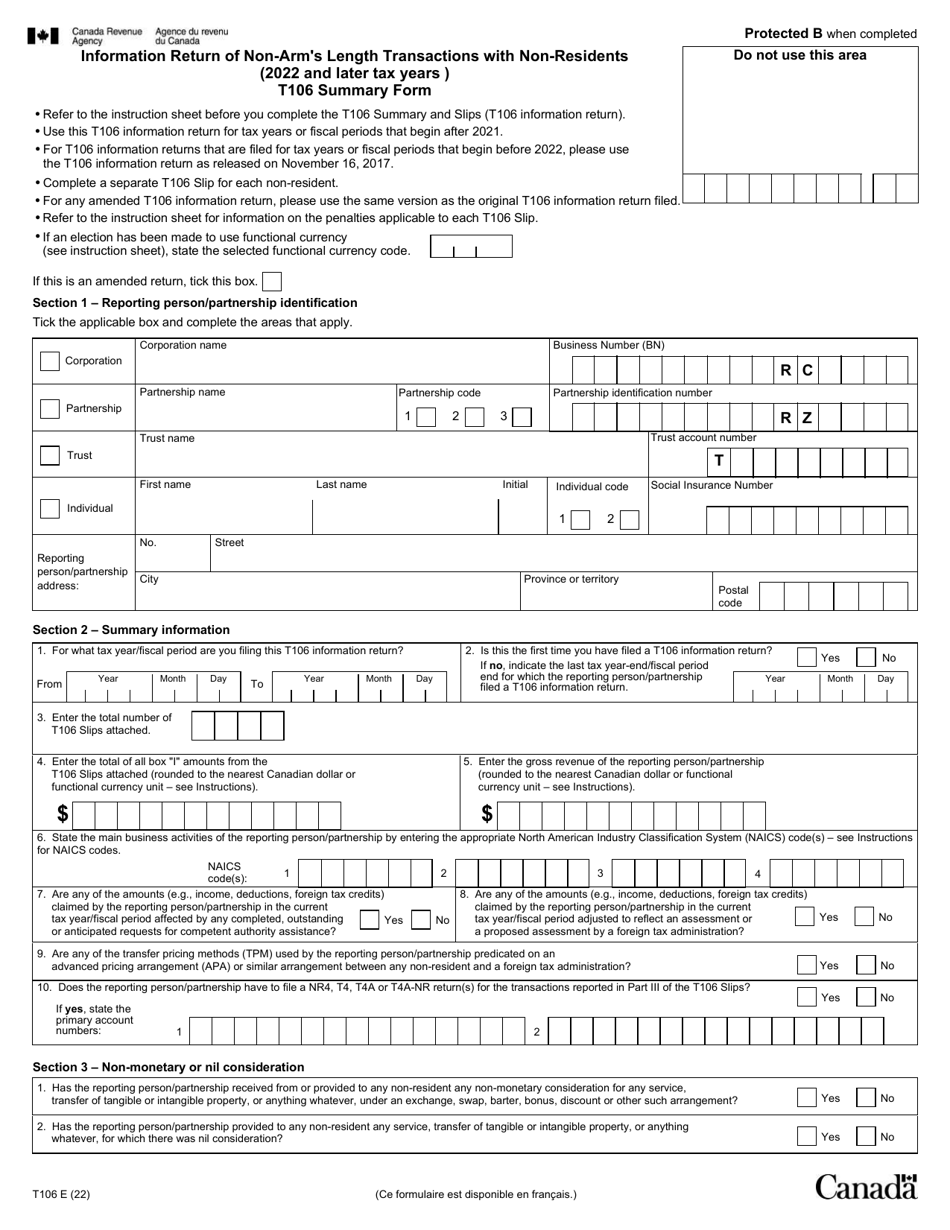

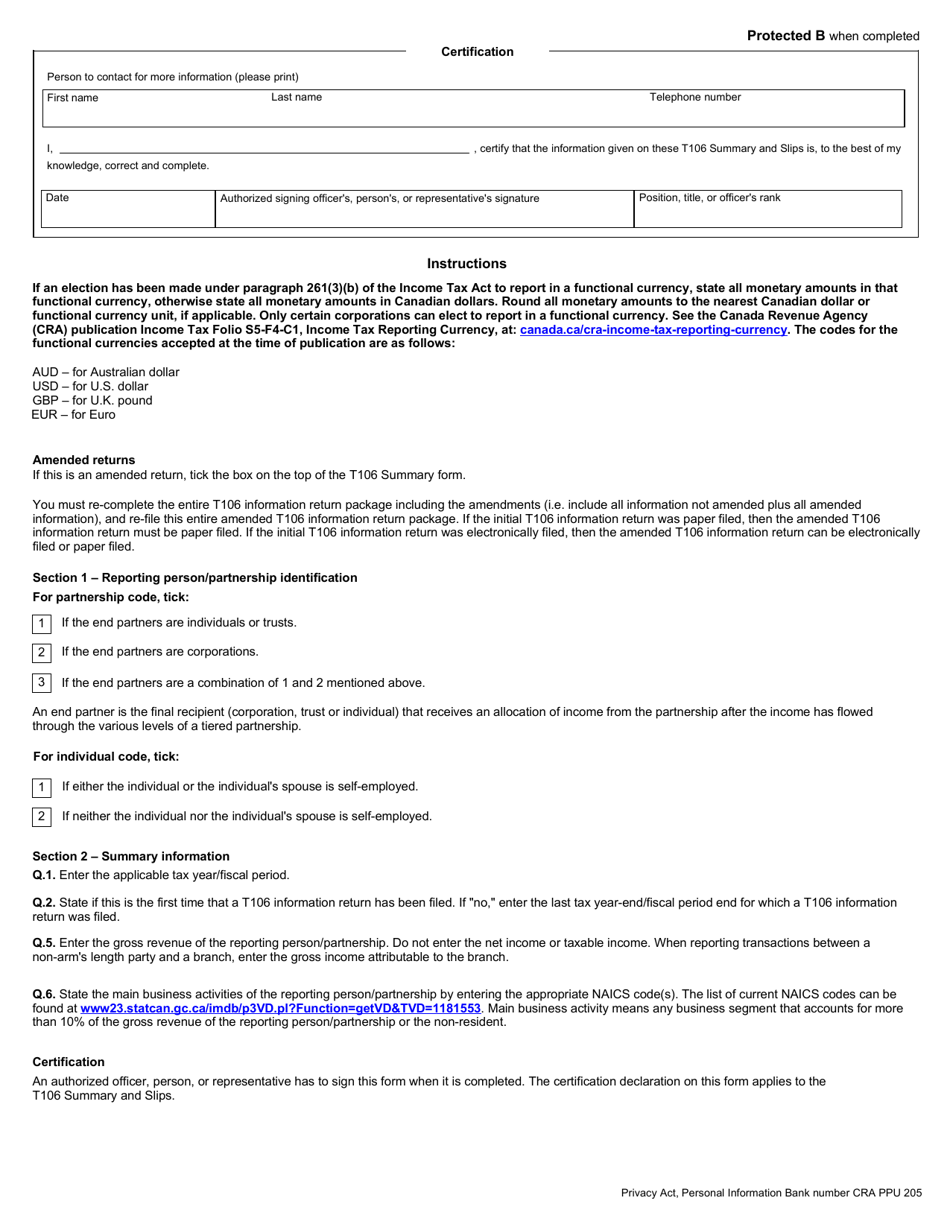

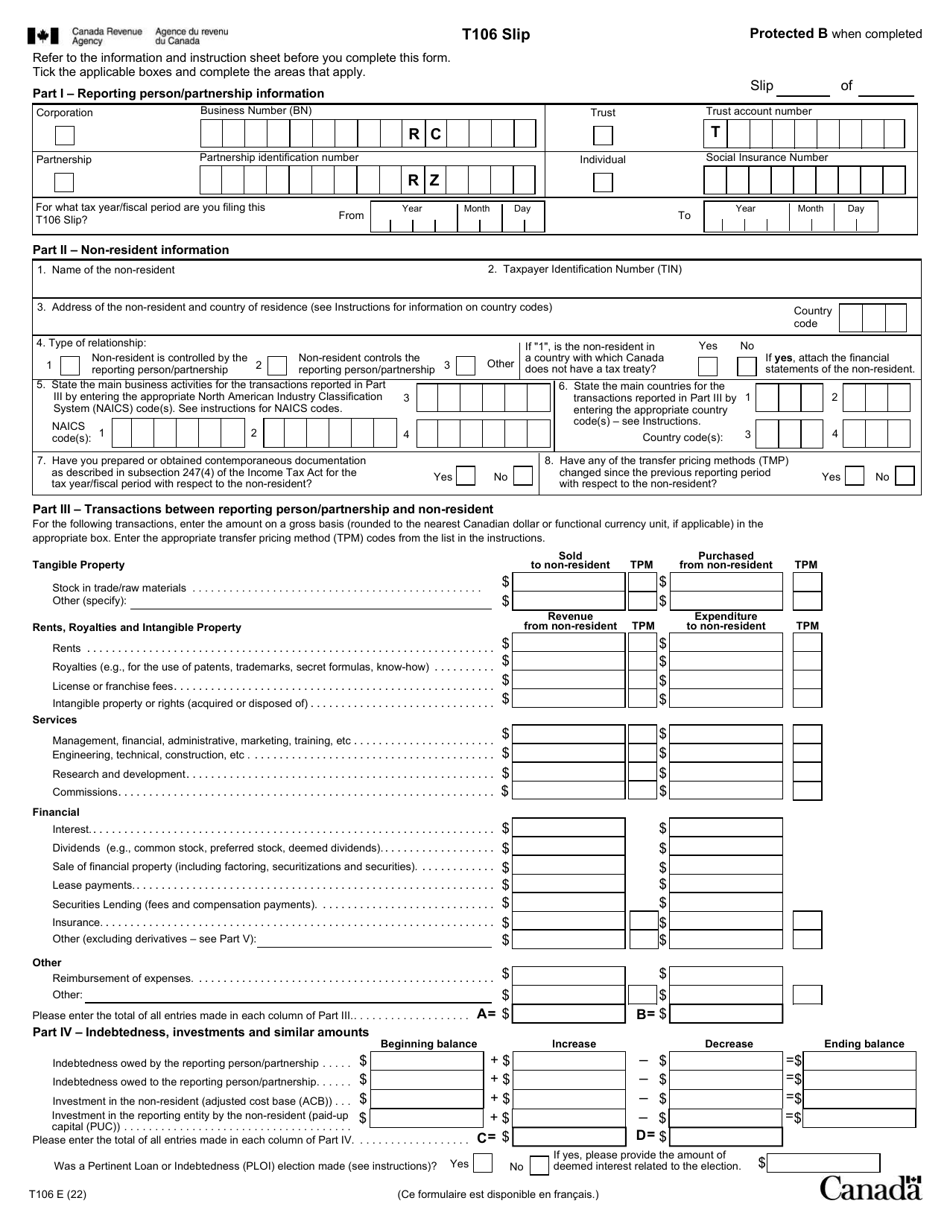

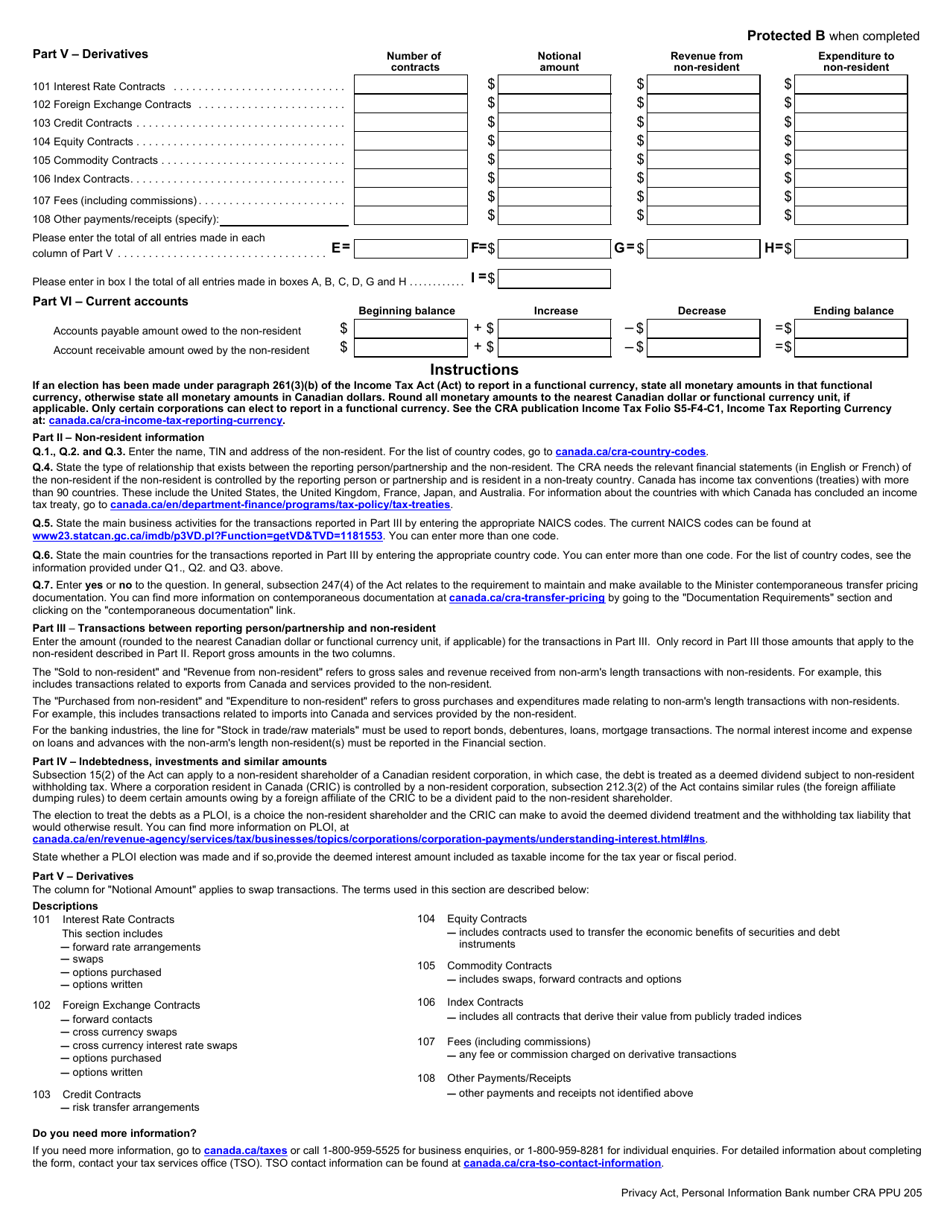

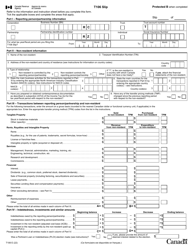

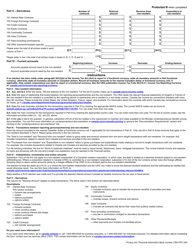

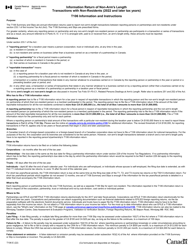

Form T106 Information Return of Non-arm's Length Transactions With Non-residents (2022 and Later Tax Years) in Canada is used to report certain transactions that Canadian residents have with non-residents with whom they have a non-arm's length relationship. It is used to provide information to the Canada Revenue Agency (CRA) about these transactions for tax purposes.

The Form T106 Information Return of Non-arm's Length Transactions With Non-residents (2022 and Later Tax Years) in Canada is filed by taxpayers who have engaged in non-arm's length transactions with non-residents.

FAQ

Q: What is Form T106?

A: Form T106 is an information return used to report non-arm's length transactions with non-residents for tax years 2022 and onwards in Canada.

Q: Who needs to file Form T106?

A: Any taxpayer in Canada who has engaged in non-arm's length transactions with non-residents needs to file Form T106.

Q: What are non-arm's length transactions?

A: Non-arm's length transactions are transactions between related parties, such as family members or businesses with common ownership.

Q: What information is required on Form T106?

A: Form T106 requires detailed information about the non-arm's length transactions, including the nature of the transactions, amounts involved, and the identities of the parties.

Q: When is Form T106 due?

A: Form T106 is due on the same date as the taxpayer's income tax return, which is generally April 30th of the year following the tax year.

Q: Does Form T106 apply only to residents of Canada?

A: No, Form T106 applies to any taxpayer in Canada, including both residents and non-residents, who have engaged in non-arm's length transactions with non-residents.

Q: Are there any penalties for not filing Form T106?

A: Yes, there can be penalties for not filing Form T106 or for filing it incorrectly. It is important to comply with the filing requirements to avoid these penalties.

Download Form T106 Information Return of Non-arm's Length Transactions With Non-residents (2022 and Later Tax Years) - Canada

1

2

3

4

5

6