![]() This version of the form is not currently in use and is provided for reference only. Download this version of

Form 561

for the current year.

This version of the form is not currently in use and is provided for reference only. Download this version of

Form 561

for the current year.

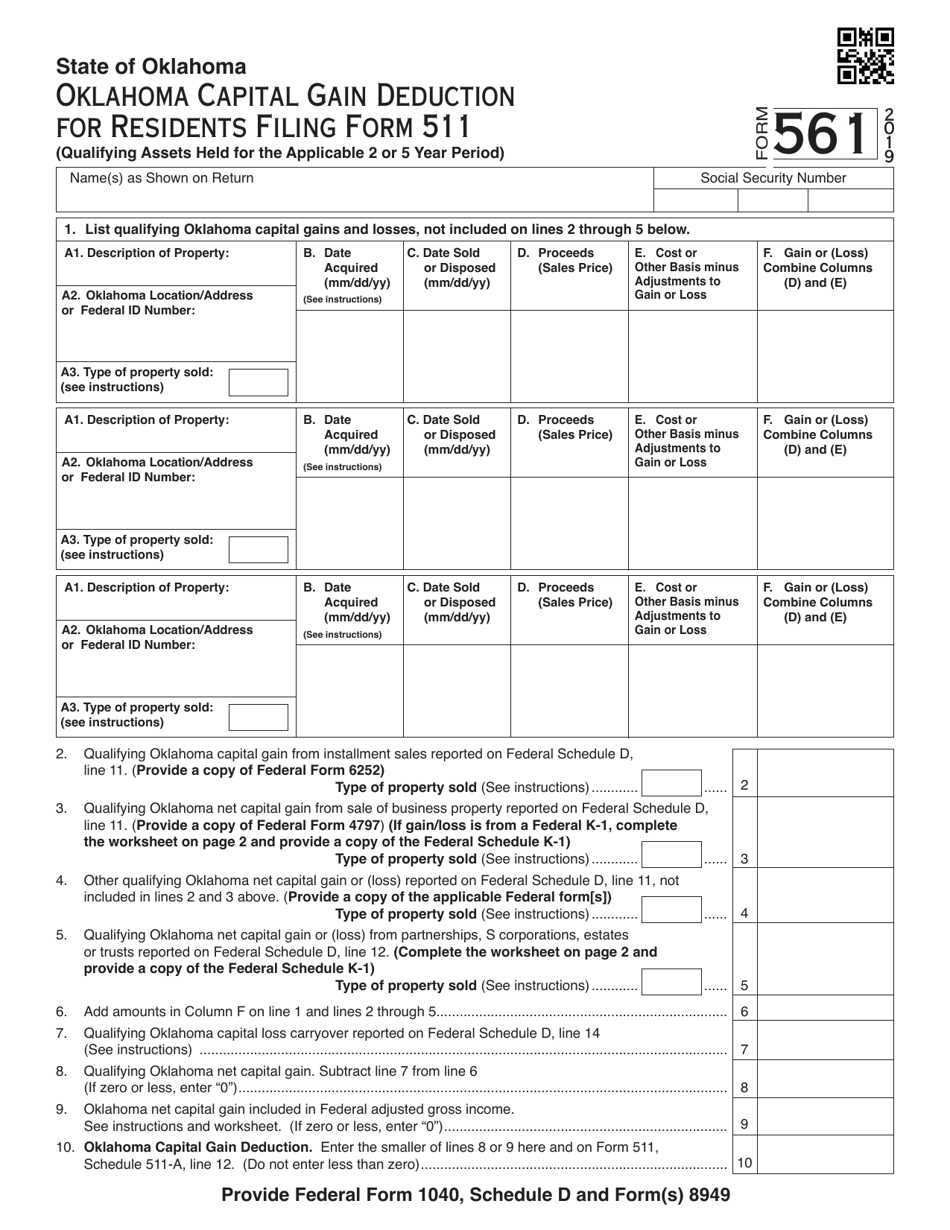

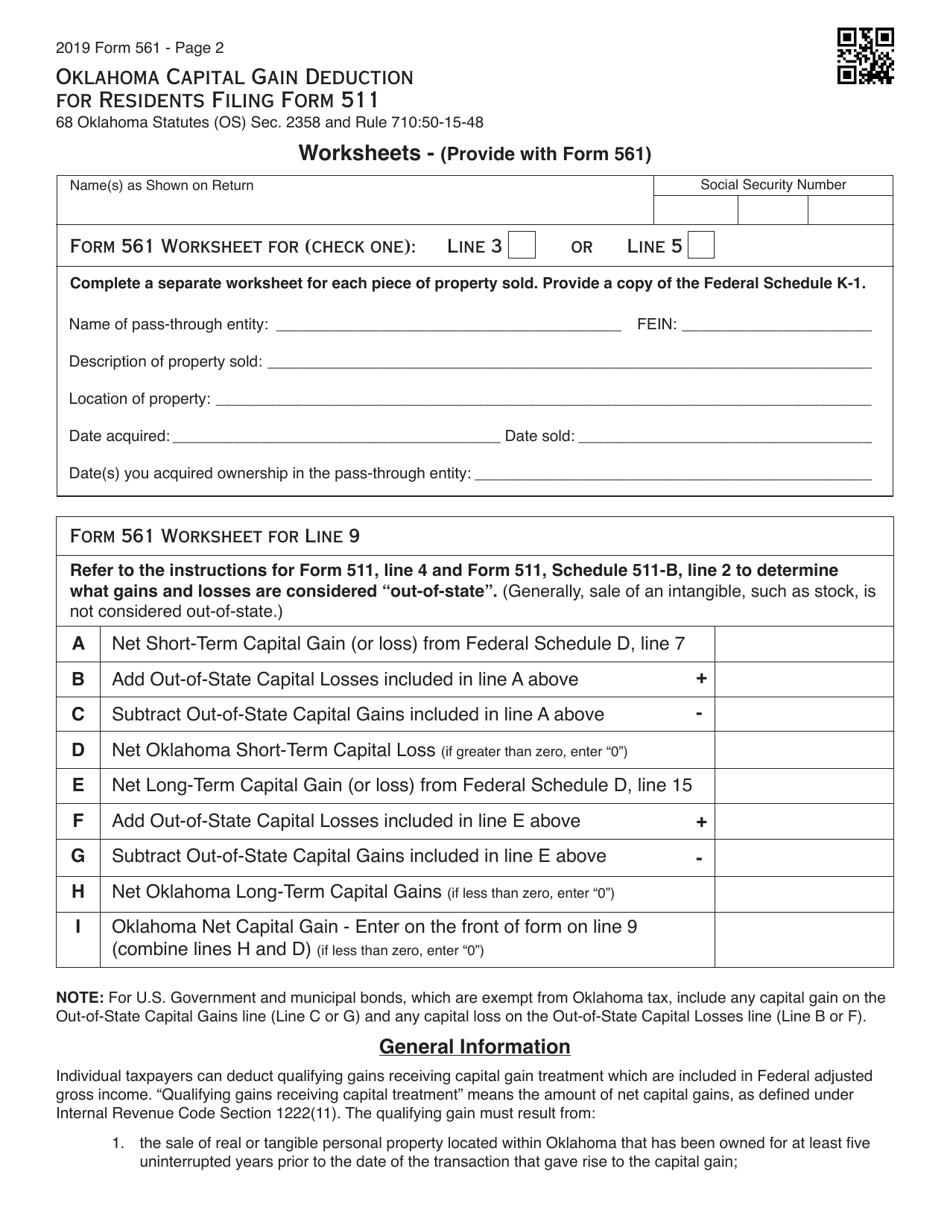

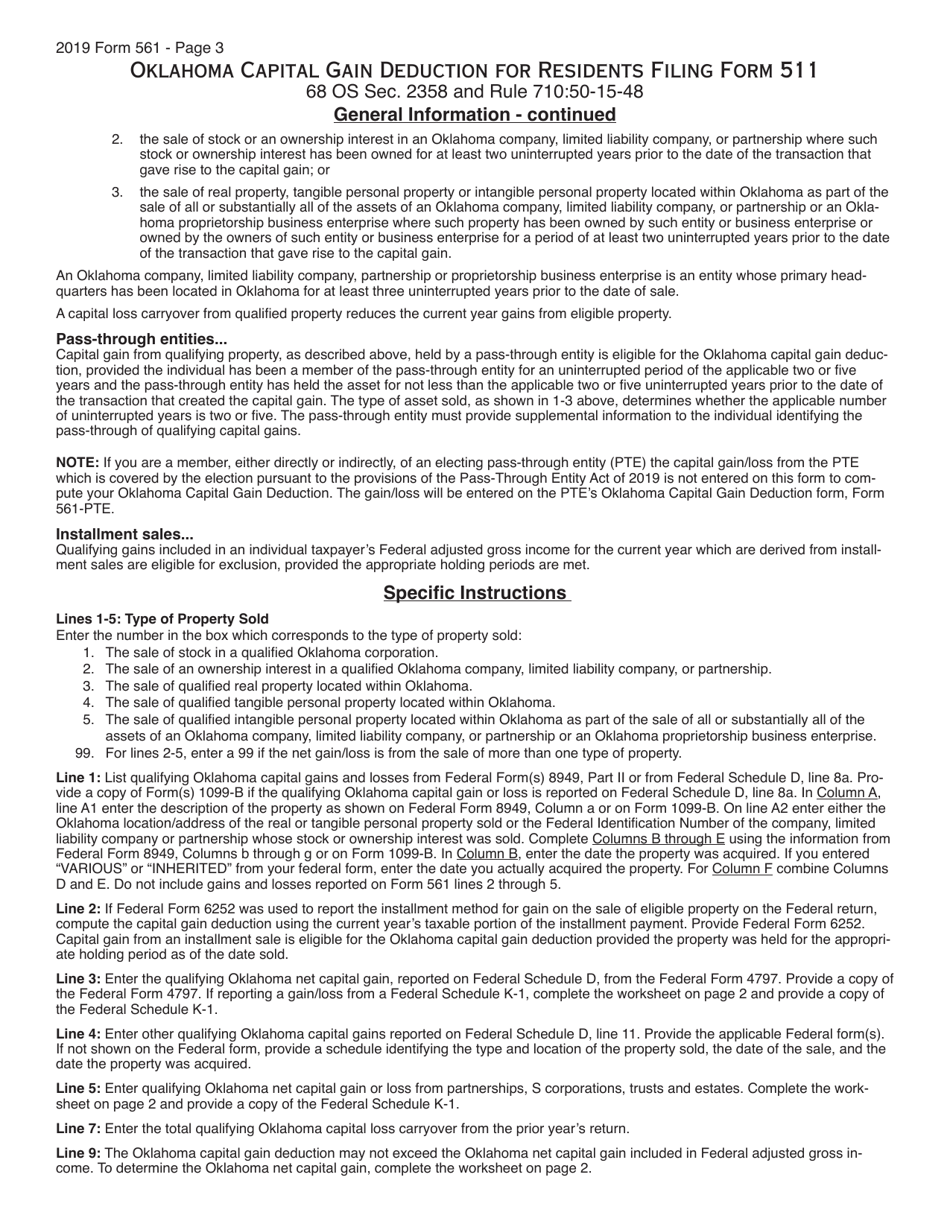

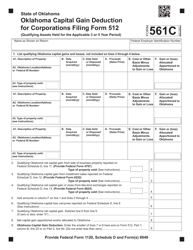

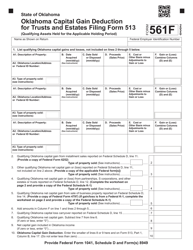

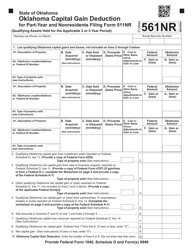

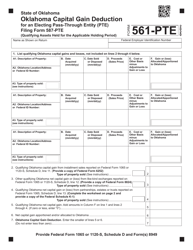

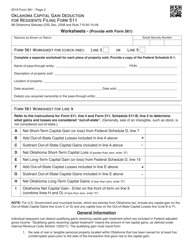

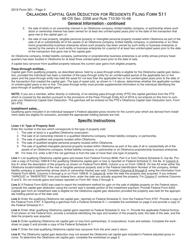

Form 561 Oklahoma Capital Gain Deduction for Residents Filing Form 511 - Oklahoma

What Is Form 561?

This is a legal form that was released by the Oklahoma Tax Commission - a government authority operating within Oklahoma. As of today, no separate filing guidelines for the form are provided by the issuing department.

FAQ

Q: What is Form 561?

A: Form 561 is a tax form in Oklahoma that allows residents to claim a capital gain deduction when filing Form 511.

Q: Who can use Form 561?

A: Form 561 can be used by residents of Oklahoma who are filing Form 511 and have capital gains to report.

Q: What is the purpose of Form 561?

A: The purpose of Form 561 is to provide a deduction for capital gains on the Oklahoma state tax return.

Q: Are there any eligibility requirements for using Form 561?

A: Yes, to use Form 561, you must be a resident of Oklahoma and have capital gains to report on your Form 511.

Q: How do I fill out Form 561?

A: To fill out Form 561, you will need to enter your personal information, calculate your capital gain deduction, and include it with your Form 511.

Q: Is there a deadline for filing Form 561?

A: Yes, Form 561 should be filed along with your Form 511 by the due date of your state income tax return.

Q: Can I claim the capital gain deduction on my federal tax return?

A: No, the capital gain deduction on Form 561 is specific to the Oklahoma state tax return and cannot be claimed on the federal tax return.

Q: What documentation do I need to support my capital gain deduction?

A: You should keep records of your capital gains, such as investment statements and sales records, to support your deduction on Form 561.

Q: Is there a limit to the amount of capital gain deduction I can claim?

A: There is no limit to the amount of capital gain deduction you can claim on Form 561, as long as you have eligible capital gains to report.

Form Details:

- The latest edition provided by the Oklahoma Tax Commission;

- Easy to use and ready to print;

- Quick to customize;

- Compatible with most PDF-viewing applications;

- Fill out the form in our online filing application.

Download a fillable version of Form 561 by clicking the link below or browse more documents and templates provided by the Oklahoma Tax Commission.

Download Form 561 Oklahoma Capital Gain Deduction for Residents Filing Form 511 - Oklahoma

1

2

3